Table of Contents

Introduction

Ever bought something on EMI thinking “just ₹3,499/month is easy” only to realize months later you’re drowning in debt? You’re not alone. This is emi trap psychology at work: the hidden mental tricks that make poor people feel rich while quietly destroying their financial future. Your brain focuses on small monthly payments instead of the total cost, creating a false sense of affordability. In India alone, millions get stuck in cycles of debt because EMIs feel painless until it’s too late. The good news? You can break free once you understand the 7 psychological spending traps behind this phenomenon.

What Is the emi trap psychology Behind Spending?

emi trap psychology refers to the cognitive biases and mental shortcuts that make people overspend using Equated Monthly Installments. When you pay via EMI, your brain perceives the cost as “small” and “manageable,” even when the total amount is far beyond your means. This illusion is especially dangerous for low-income earners who feel richer temporarily but end up poorer long-term.

According to financial experts, the average Indian household now holds over ₹20 lakh crore in consumer durable and personal loan EMIs a 40% rise in just 3 years. The problem isn’t EMI itself; it’s how our psychology tricks us into using it poorly.

Understanding emi trap psychology is the first step toward smarter money decisions. Let’s break down the 7 most common traps.

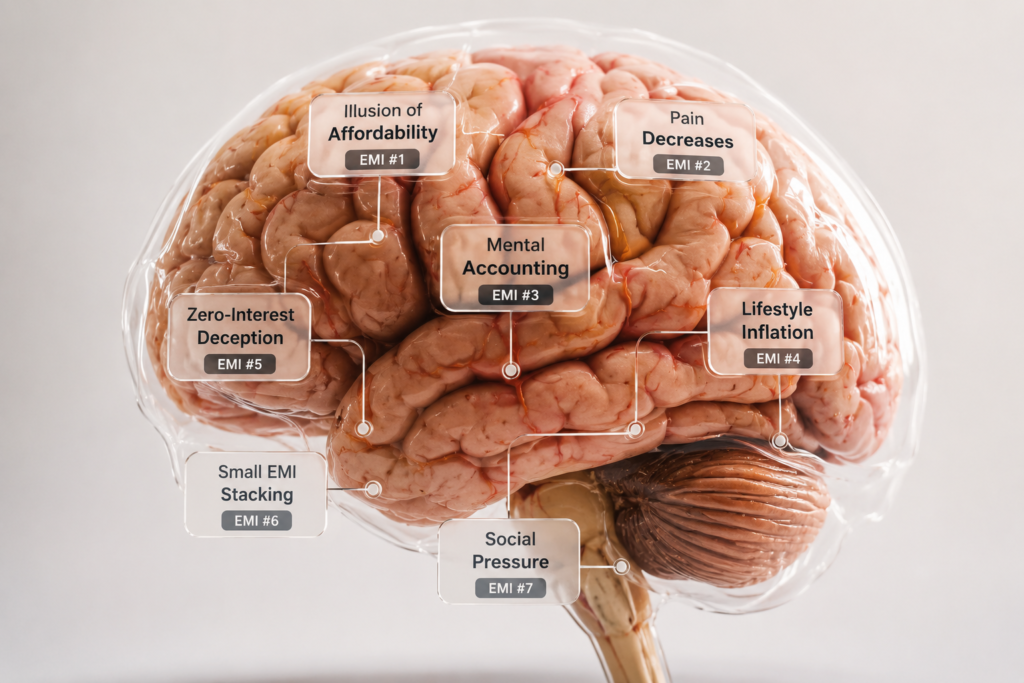

7 Psychological Spending Traps Explained Simply

Trap 1: The Illusion of Affordability

Your brain asks “Can I afford ₹4,999/month?” instead of “Can I afford ₹59,888 total?” This frames expensive items as affordable, triggering purchase decisions you’d never make if paying cash.

Trap 2: Pain of Payment Decreases

Cash spending feels painful — you physically hand over money. EMI spreads that pain across months, making each payment feel negligible. Studies show people spend 30–40% more when using installment plans.

Trap 3: Mental Accounting Bias

You mentally separate “EMI money” from “savings money.” Even though it’s the same income, you treat future EMI payments as someone else’s problem — your future self’s problem.

Trap 4: Lifestyle Inflation Sneak Attack

Each new EMI raises your lifestyle baseline. That new phone, TV, or sofa becomes “normal,” pushing you to take more EMIs to maintain the illusion of wealth.

Trap 5: Zero-Interest EMI Deception

“Zero interest” sounds amazing — but processing fees, insurance, and lost cash discounts add up. Many zero-interest EMIs cost 8–12% effective interest after hidden charges.

Trap 6: Small EMI Stacking Effect

₹1,999 + ₹2,499 + ₹3,999 seems manageable alone. But 5–6 small EMIs can consume 50%+ of your take-home pay without you noticing until it’s too late.

Trap 7: Social Pressure and FOMO

Seeing friends with the latest iPhone or SUV creates pressure to “keep up.” EMIs make luxury accessible now, but the debt lasts years. This is especially painful for low-income groups chasing dignity and social status.

EMI Trap Psychology vs Cash Spending: Key Differences

| Factor | EMI Spending | Cash Spending |

|---|---|---|

| Pain of payment | Low (spread out) | High (immediate) |

| Total cost awareness | Low (focus on monthly) | High (full price visible) |

| Overspending risk | 3–4× higher | Minimal |

| Emotional satisfaction | Temporary (instant) | Lasting (no debt stress) |

| Impact on savings | Reduces future flexibility | Preserves capital |

| Debt accumulation | High (compounding) | None |

| Financial freedom | Delays it | Builds it |

This table shows why emi trap psychology is so dangerous it hides the real cost while making you feel rich today.

Pros and Cons

Pros

Makes essential high-cost items accessible (e.g., medical emergencies, education)

Builds credit history when paid on time

Allows cash flow management for verified assets

Some offers include warranty or insurance benefits

Cons

Creates false sense of affordability

Total cost often 20–40% higher than cash price

Reduces future income flexibility

Triggers lifestyle inflation

High risk of debt trap for low-income earners

Hidden fees in “zero-interest” offers

Psychological stress from looming payments

How to Break the emi trap psychology Cycle

Ready to escape? Follow these 7 actionable steps:

Wait 30 days before any non-essential EMI purchase — delays reveal true need

Calculate total cost including interest, fees, and lost discounts before signing

Limit total EMIs to 30–35% of your net monthly income

Avoid multiple small EMIs — they stack dangerously fast

Prefer down-payment + shorter tenure if EMI is unavoidable

Build emergency fund first before taking any EMI commitment

Ask: “Do I need this or want this?” — be brutally honest

For more smart money strategies, visit https://nextgendecode.in/.

Conclusion

emi trap psychology isn’t about being bad with money it’s about your brain being wired to prefer present joy over future security. The 7 traps we covered explain why poor people feel rich temporarily but end up trapped in debt. The solution? Slow down, calculate total costs, limit EMIs, and prioritize cash spending for non-essentials. Remember: when it comes to wealth-building, small leaks sink big ships. Start today your future self will thank you.

FAQ Section

Question 1:Why does EMI make me feel richer than paying cash?

EMI reduces the pain of payment by spreading cost across months. Your brain focuses on small monthly amounts instead of total price, creating false affordability.

Question 2:Are zero-interest EMIs really free?

No. They include processing fees, insurance, and inflated base prices. Effective interest often reaches 8–12% after hidden charges.

Question 3:What percentage of income should go to EMIs?

Financial experts recommend keeping total EMIs under 30–35% of net monthly income to avoid debt traps.

Question 4:How do I break EMI addiction completely?

Start with a 30-day wait rule, track all expenses weekly, build an emergency fund, and switch to cash-based goals for non-essentials.