Table of Contents

Introduction: The Money Decisions Your Future Self Will Thank You For

I remember being 23 and thinking, “I will figure out money later.” Later came fast. And it brought credit card debt, zero savings, and a lot of regret.

The truth is that money habits in your 20s shape nearly everything that follows. The way you spend, save, and think about money right now is quietly writing the first chapter of your financial story. And the good news? You still have time to make it a great one.

This post covers 8 proven habits that actually work, why they matter more than most people realize, and how to start building them today even if you feel behind right now. No fluff, no complicated jargon, just real, actionable steps.

The 8 Money Habits in Your 20s That Actually Change Everything

These are not abstract tips. These are specific, daily decisions that quietly compound into life-changing results.

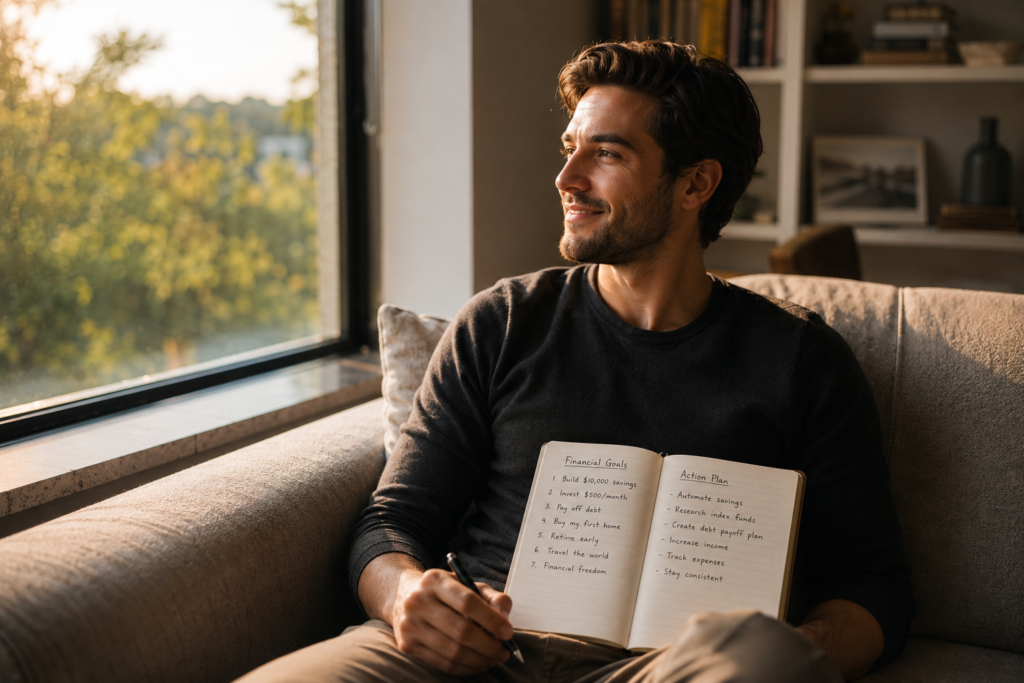

Start a Budget and Actually Stick to It

Most people in their 20s have no idea where their money goes. A budget fixes that. Start with the 50/30/20 rule: 50% for needs, 30% for wants, and 20% for savings and debt. You do not need a perfect spreadsheet. Even a basic notes app works if you use it consistently. The habit matters more than the tool.

Build an Emergency Fund First

Before investing, before splurging, before anything else, build an emergency fund. Aim for 3 to 6 months of living expenses in a separate savings account. This is the habit that stops one bad week from turning into years of debt. According to Investopedia, an emergency fund is the cornerstone of any solid financial plan.

Pay Yourself Before Anyone Else

This is one of the most powerful money habits in your 20s: automate your savings before you ever see the money. Set up an automatic transfer to your savings or investment account on payday. When saving happens automatically, you never feel the temptation to skip it. Even saving 10% of every paycheck adds up to something meaningful over time.

Avoid Lifestyle Inflation Like the Plague

You get a raise. So you upgrade your apartment, your car, your wardrobe. This is called lifestyle inflation and it silently kills financial progress for millions of people. Every time your income goes up, resist the urge to match it with spending. Instead, direct a portion of every raise directly into savings or investments. Your future self will not miss the extra lattes.

Start Investing Even If It Feels Too Early

The biggest investing myth in your 20s is that you need a lot of money to start. You do not. Even investing 50 to 100 dollars a month in a simple index fund creates a foundation that compounds massively over decades. NerdWallet explains clearly how starting early, even with small amounts, produces dramatically better results than starting later with larger ones.

Tackle Debt Before It Tackles You

Not all debt is equal. High-interest debt like credit cards is a financial emergency. Pay those off aggressively using either the avalanche method (highest interest first) or the snowball method (smallest balance first). Student loans and mortgages are different stories but still need a clear payoff plan. Debt with no strategy is like a slow leak in a tire: you barely notice until you are completely stuck.

Learn About Money Consistently

Financial literacy is a habit, not a one-time event. Read one finance book per quarter. Follow credible personal finance sources. Listen to money podcasts during your commute. The more you understand how money actually works, the better every decision you make becomes. Knowledge compounds just like interest does.

Protect Yourself With the Right Insurance

Nobody in their 20s wants to think about insurance. But one unexpected medical bill, accident, or disability without coverage can erase years of savings overnight. Make sure you have health insurance, renter’s insurance, and at least some basic life insurance if others depend on you. These are not exciting purchases, but they protect every other financial habit you are building.

Why Money Habits in Your 20s Matter More Than You Think

Here is the honest reason this decade matters so much: compound interest.

When you invest or save at 22, every dollar has 40-plus years to grow. At 35, it has 25. That difference is not just big, it is the difference between retiring comfortably and working longer than you ever wanted to.

Beyond math, your 20s are when your financial identity is being formed. The habits, beliefs, and patterns you build right now become automatic behaviors by your 30s. Most people do not realize this until they look back and wish they had started sooner.

Building strong money habits now does not mean depriving yourself. It means making deliberate choices so that future-you has options.

Good Habits vs. Bad Habits: A Comparison

| Habit | What It Looks Like Now | What It Creates by 40 |

|---|---|---|

| Budgeting monthly | Takes 30 minutes a week | Full financial awareness and control |

| No budget at all | Feels free short-term | Confusion, overspending, zero savings |

| Investing 100 dollars monthly | Feels small and slow | 60,000 to 100,000 dollars or more (at 8% return over 20 years) |

| Spending every paycheck | Feels normal | No cushion, no options, high stress |

| Emergency fund in place | Peace of mind, boring | Stability when life gets hard |

| No emergency fund | Fine until it is not | One crisis becomes a financial spiral |

| Avoiding lifestyle inflation | Requires discipline | Real wealth accumulation over time |

| Upgrading with every raise | Feels rewarding now | Income goes up, savings stay zero |

Pros and Cons of Building Financial Habits Early

Pros of Building Money Habits Early

- Compound growth works in your favor for decades when you start young.

- Lower financial stress because you have a plan and a safety net.

- More options in your 30s and 40s: career changes, travel, early retirement become real possibilities.

- Debt stays manageable because you attack it early with a strategy.

- Confidence increases as you watch your savings and investments grow over time.

Cons of Building Money Habits Early

- Requires sacrifice that friends around you may not be making, which can feel isolating.

- Learning curve is real: financial literacy takes consistent effort and does not come naturally to everyone.

- Mistakes are part of the process: bad investments or spending relapses are common, especially early on.

- Delayed gratification is hard: it can feel like you are working toward something invisible for years.

Practical Guide: How to Start Today

You do not need to fix everything at once. Start here:

- This week: Open a separate savings account and name it “Emergency Fund.” Even 500 dollars starts the habit.

- This month: Track every expense for 30 days. No judgment, just data. Then make your first real budget.

- This quarter: Research and open a basic investment account. Index funds are a beginner-friendly place to start.

- This year: Set a goal to pay off your highest-interest debt or increase your savings rate by 5%.

- Ongoing: Read or listen to one credible personal finance resource every month. Stay curious and stay consistent.

For more guides on building smart financial and digital habits, visit NextGenDecode.in and explore our full resource library.

These Small Choices Build a Bigger Life

None of these habits are complicated. None of them require a finance degree or a six-figure salary. What they require is consistency over time, and the willingness to care about your future a little more than your present comfort.

The 8 money habits in your 20s covered here (budgeting, emergency savings, paying yourself first, avoiding lifestyle inflation, investing early, attacking debt, learning consistently, and protecting yourself with insurance) are not shortcuts. They are foundations. Build them right and everything else becomes easier.

Pick one habit from this list and start it this week. Not next month. Not when things settle down. This week. Small, consistent steps taken now create the financial freedom that most people only wish they had later.

Frequently Asked Questions About Money Habits in Your 20s

What are the most important money habits in your 20s?

The three most critical money habits in your 20s are building an emergency fund, starting to invest early (even small amounts), and sticking to a monthly budget. These three alone can dramatically change your financial trajectory. Everything else builds on top of them.

How much should I save in my 20s?

A good starting target is saving at least 20% of your monthly take-home income. If that feels too high right now, start with 10% and work up gradually. The exact amount matters less than the consistency of saving something every single month without fail.

Is it too late to start good money habits at 25 or 28?

Not at all. Starting at 25 or 28 still gives you decades of compound growth, plenty of time to eliminate debt, and years to build real savings. The best time was five years ago. The second best time is right now. Do not let the feeling of being “behind” stop you from starting.

What happens if I ignore my finances in my 20s?

Ignoring your finances in your 20s typically leads to high-interest debt, zero savings cushion, missed years of investment growth, and significantly more financial stress in your 30s and 40s. It is not impossible to recover, but every year you delay makes the path longer and harder.